Physical AI and Robotics Shift Toward Commercial Deployment

Investment Research

July, 2026

Physical AI is moving robotics from fixed automation to adaptive real-world execution. For PE and VC investors, returns will depend on capability maturity, deployment repeatability, customer validation, and measurable operating impact.

Physical AI is becoming a more relevant investment theme as enterprises reassess automation priorities across labor, productivity, safety, and operational flexibility. For investors, the category should be evaluated through commercial readiness rather than broad technology visibility. The stronger opportunity lies with companies that will likely demonstrate implementation depth, clear customer economics, and the ability to scale validated use cases across operating environments.

Enterprise Adoption Moves Toward Measurable Operating Value

Enterprise interest in physical AI is increasingly linked to business outcomes. Around 67% of executives view Physical AI as game-changing for their industry, while 79% are already engaging with physical AI today, as per Capgemini. Around 60% also believe it will enable robotics adoption in areas previously considered impossible or impractical, including unstructured environments, context-dependent tasks, and autonomous adaptation across operating settings.

This demand profile gives the category a stronger commercial foundation than many early-stage technology themes. Enterprises are evaluating physical AI because it is relevant to productivity, resilience, safety, and operating flexibility. For investors, that distinction is important. The most attractive companies will be those that translate these enterprise priorities into reliable deployments, visible ROI, customer proof, and scalable go-to-market models across sectors.

Read more: US VC in Transition: Valuations Reset, Returns Uneven

Physical AI Expands the Commercial Scope of Robotics

Physical AI applies AI to physical systems, enabling machines to perceive, reason, and act autonomously in real-world environments. In robotics, its relevance spans industrial robot arms, autonomous mobile robots, cobots, humanoids, quadrupeds, drones, and special-purpose robots. It also expands robotic capability across perception, adaptability, autonomy, learning capability, generalization, collective learning, and natural-language understanding.

The investment implication is that physical AI should be viewed as more than a hardware upgrade cycle. The broader opportunity is tied to transferable intelligence across machines, tasks, and operating settings. As robotic systems become more adaptive, the value pool will likely expand beyond isolated automation use cases toward scalable deployment models. Long-term advantage is likely to sit with companies that improve system performance across customer environments.

Capability Maturity Becomes Central to Robotics Diligence

The humanoid robotics market has attracted significant attention, with 2030 projections ranging from under 1 million annual units to more than 6 million, as per BCG. However, the capabilities required for broad deployment are maturing at different speeds across the robotics stack. Progress in perception, dexterity, planning, and reasoning remains uneven, while true general-purpose autonomy remains largely aspirational within the most advanced maturity framework.

This creates an important diligence requirement for investors. A human-like form factor should not be treated as evidence of broad commercial capability. The more relevant questions are whether the system will likely perform valuable work reliably, operate under real-world variability, integrate into customer workflows, and support a clear implementation case. Investors should focus on capability maturity, implementation complexity, unit economics, and evidence of recurring demand.

Read more: Medtech VC & PE Trends 2026: Investors Prioritize Scale, Liquidity, and Commercial Traction

Robotics Funding Shifts Toward Scale and Customer Validation

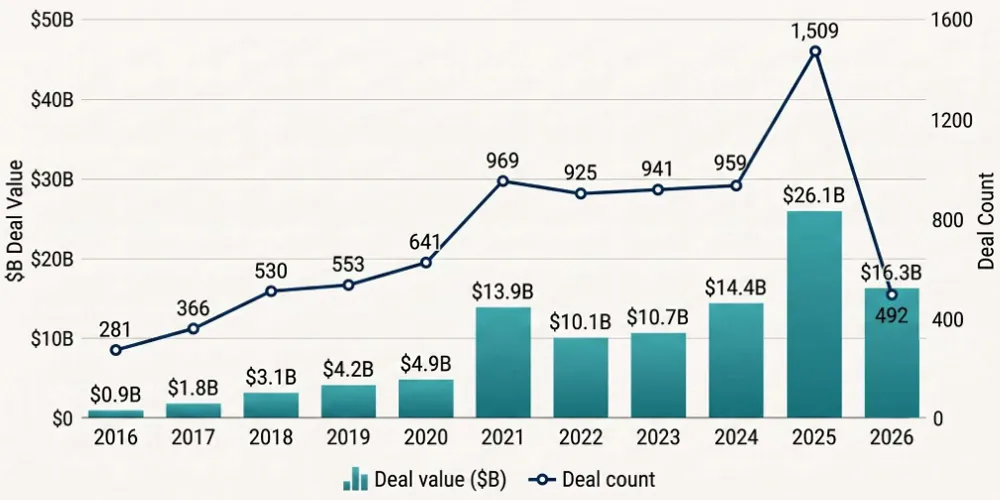

Global robotics and physical AI startups raised $16.3 billion across 492 deals in 1Q26, marking the strongest quarter on record by both value and deal count, as per PitchBook. Deal value increased 154% QoQ and 256% YoY. Three large rounds, Shield AI at $1.5 billion, Saronic at $1.8 billion, and Neura Robotics up to $1.4 billion, underscore the role of scaled companies in driving quarterly funding momentum.

Figure 1: Global Robotics & Physical AI VC Deal Activity

Source: PitchBook, data as of March 31, 2026

The funding environment indicates that investor attention remains strong, but diligence is becoming more demanding. Capital is increasingly being directed toward companies that will likely show scale, paying customers, repeat orders, and deployment durability. This shift is constructive for the sector. Robotics businesses often face long sales cycles, integration complexity, and customer-specific implementation requirements, making scalable deployment models increasingly important.

Industrial Robotics Gains Relevance in Capital Allocation

Industrial robotics reached $5.6 billion across 118 deals in 1Q26 and $10.8 billion on a trailing 12-month (TTM) basis, placing it within 10% of defense and security robotics, as per PitchBook. Moreover, defense and security robotics attracted $4.5 billion in 1Q across 101 deals, bringing TTM to $11.9 billion. Assembly and manufacturing robots reached $7.8 billion TTM, reinforcing the segment’s momentum.

This segment is likely to remain central to the investment case for physical AI because industrial environments offer clearer ROI, defined workflows, and large deployment bases. The opportunity is not limited to robot manufacturers. It extends to enabling software, systems integration, automation services, components, workflow orchestration, and vertical-specific deployment models, creating opportunities for both venture-scale platforms and private equity-led consolidation.

Conclusion

Physical AI represents a meaningful evolution in robotics, but the investment case will depend on execution quality rather than category momentum alone. The market is likely to reward companies that combine proven execution, deployment discipline, visible adoption economics, and software layers that reduce integration complexity. Durable value creation is more likely to come from businesses solving specific industrial, logistics, manufacturing, and service automation challenges.

About SG Analytics

SG Analytics (SGA) is a global leader in data-driven research and analytics, empowering Fortune 500 clients across BFSI, Technology, Media & Entertainment, and Healthcare. A trusted partner for lower middle market investment banks and private equity firms, SGA provides offshore analysts with seamless deal life cycle support. Our integrated back-office research ecosystem, including database access, design support, domain experts, and tech-enabled automation, helps clients win more mandates and execute deals with precision.

Founded in 2007, SGA is a Great Place to Work® certified firm with 1,600+ employees across the U.S., the UK, Switzerland, Poland, and India. Recognized by Gartner, Everest Group, and ISG and featured in the Deloitte Technology Fast 50 India 2023 and Financial Times APAC 2024 High Growth Companies, we continue to set industry benchmarks in data excellence.

Related Tags

Author

Steve Salvius

Head of Investment Banking & Private Equity