US VC Midyear Outlook 2026: Liquidity and Portfolio Quality Define the Recovery

Private Equity

July, 2026

Venture capital (VC) activity is recovering unevenly, with capital concentrated around stronger companies, selective liquidity channels, and defensible technology exposure. For investors, allocation will depend less on momentum and more on formation quality, exit visibility, and portfolio resilience.

The US VC market at midyear 2026 remains far from broad normalization. Company formation is improving, late-stage capital remains available, and liquidity channels are reopening selectively. However, capital continues to flow toward stronger managers, category leaders, and companies linked to durable technology demand. For investors, the priority is to identify where growth quality, business durability, and liquidity visibility will likely translate into returns.

Lower Formation Costs Reopen Early-Stage Venture Activity

US first-financing activity was tracking to exceed 7,000 deals by year-end, based on data as of May 31, 2026, which would represent the highest annual number by more than 1,300 deals, as per PitchBook. Even without an estimated deal count, the year was on pace for nearly 6,000 first financings. Startup formation has also become easier as Claude Code and OpenAI’s Codex reduced barriers for untrained coders, while solo C-Corp formations through Stripe Atlas reached 63% in 2Q.

The early-stage funnel is reopening, but higher formation does not automatically improve return quality. Lower startup creation costs are expected to expand the number of companies entering the market, but they are also expected to increase undifferentiated opportunities across crowded categories. Stronger early-stage investors will identify customer urgency, technical depth, and founder execution velocity before shallow ideas attract excess capital.

Read more: Medtech VC & PE Trends 2026: Investors Prioritize Scale, Liquidity, and Commercial Traction

Late-Stage Capital Remains Concentrated Around Scaled Companies

US late-stage activity has remained resilient, but capital is still concentrated around scaled companies. As of May 31, 2026, $59.3 billion had been deployed across an estimated 1,990 late-stage deals, putting annualized value on pace for the second-highest level in a decade, as per PitchBook. Venture-growth activity was stronger, with $274.2 billion deployed across 409 estimated deals. The four largest rounds accounted for 86.4% of the total YTD deal value.

The late-stage market is improving unevenly. Capital remains available for companies with category leadership, growth visibility, and credible exit pathways. Companies dependent on prior-cycle valuations face a more difficult financing environment. Aggregate deal value will likely make the market appear healthier than it is. The real test is whether companies are able to justify valuations through revenue durability, margin progress, and public-market readiness.

Liquidity Recovery Remains Dependent on Select Exit Channels

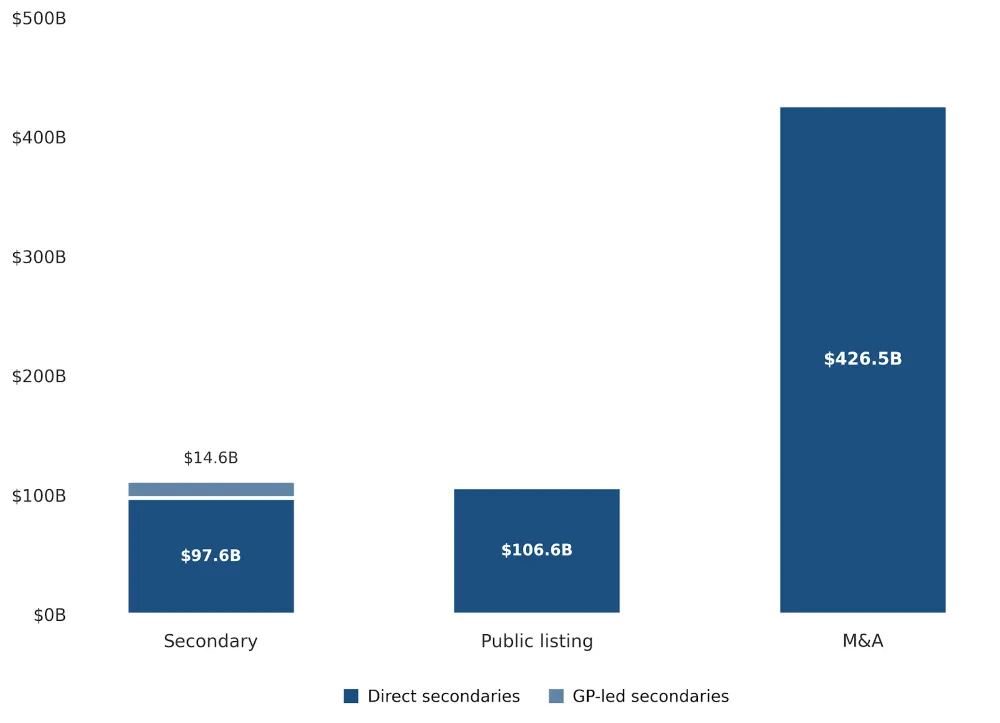

The IPO market is tracking ahead of earlier expectations, with 2026 on pace for 77 listings versus a favorable scenario of 68. US VC-backed public listings since 2016 have generated $1.5 trillion in exit value, as per PitchBook. Direct and GP-led secondaries became a more important liquidity `channel, with $97.6 billion and $14.6 billion recorded from 2Q25 to 1Q26. In May, the top 20 names accounted for 81.1% of secondary trading value.

Figure 1: US VC exit value by type (in $Billions), 2Q25-1Q26

Source: PitchBook, data as of March 31, 2026

Liquidity conditions are improving, but access remains narrow. A few high-profile exits should improve sentiment, but they do not solve the distribution gap across venture portfolios. Secondaries will remain important for funds seeking partial liquidity before exit markets normalize. The key question is whether realizations begin to move beyond the most visible companies and extend to a wider set of managers, fund vintages, and portfolio companies.

Read more: Cybersecurity VC Trends in 1Q26: Capital Concentration Shapes the Next Phase of Investment

Infrastructure Constraints Redefine Technology Investment Exposure

The US growth debate now centers on whether technology is able to expand capacity faster than constraints tighten. US real GDP per capita has historically grown at 1.9% annually, while the median technology-related growth forecast is shown at 3.5% from 2026, as per BlackRock. Scarcity remains visible across power, labor, capital, and critical materials, while the buildout requires data centers, chips, memory, and skilled labor.

For VC investors, this expands the opportunity set beyond applications. Constrained capacity is expected to shift attention toward enabling layers required for technology adoption. Infrastructure exposure matters when growth depends on power, compute, capital intensity, and physical deployment. Not every infrastructure-adjacent company will generate venture returns, but constraints will likely create pricing power, relevance, and durable demand.

Software Defensibility Becomes Central to Venture Underwriting

The pressure on software is visible in US-listed technology markets. According to J.P. Morgan, about half of the stocks in the S&P Expanded Technology Software Index are down more than 50% from all-time highs, while the median company in the index has a GAAP operating margin of just 4%. Many SaaS companies are tracked by the index, making these figures relevant to the valuation reset.

Software defensibility is a critical underwriting question for venture portfolios. Automation is expected to improve productivity, but is likely to weaken companies built on generic tools, seat-based pricing, or shallow workflow integration. Stronger software businesses will be embedded in mission-critical processes, supported by usage-based value creation and customer dependence. Investors should focus on whether new functionality strengthens retention, pricing power, and margins.

Conclusion

The VC market is becoming more active, but selectivity remains critical. Early-stage activity is expanding, late-stage capital is available, and liquidity is reopening selectively. Yet gains remain concentrated, requiring stronger underwriting discipline. The next phase of venture allocation should prioritize durability over momentum. Companies with real demand, durable economics, credible liquidity options, and structural technology exposure will be better positioned to attract capital.

About SG Analytics

SG Analytics (SGA) is a global leader in data-driven research and analytics, empowering Fortune 500 clients across BFSI, Technology, Media & Entertainment, and Healthcare. A trusted partner for lower middle market investment banks and private equity firms, SGA provides offshore analysts with seamless deal life cycle support. Our integrated back-office research ecosystem, including database access, design support, domain experts, and tech-enabled automation, helps clients win more mandates and execute deals with precision.

Founded in 2007, SGA is a Great Place to Work® certified firm with 1,600+ employees across the U.S., the UK, Switzerland, Poland, and India. Recognized by Gartner, Everest Group, and ISG and featured in the Deloitte Technology Fast 50 India 2023 and Financial Times APAC 2024 High Growth Companies, we continue to set industry benchmarks in data excellence.

Related Tags

Author

Steve Salvius

Head of Investment Banking & Private Equity