Cybersecurity VC Trends in 1Q26: Capital Concentration Shapes the Next Phase of Investment

Private Equity

June, 2026

Cybersecurity funding remains resilient, but the VC market is becoming selective. As AI reshapes enterprise security requirements and risk management priorities, investors are concentrating capital in a smaller group of AI-native platforms and security operations providers.

Cybersecurity VC entered 2026 with a familiar paradox. Funding remained resilient even as deal activity continued to decline. Rather than signaling weakness, the divergence reflects a more selective investment environment, with capital flowing toward companies demonstrating stronger differentiation and exposure to AI-driven security trends. Across the market, capital is concentrating around a smaller group of companies shaping the next phase of cybersecurity innovation.

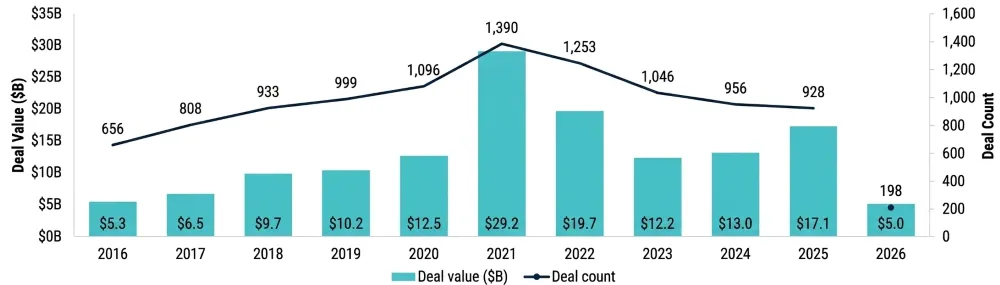

Funding Remains Resilient Despite Fewer Deals

Cybersecurity venture funding held steady at approximately $5 billion in 1Q26, while deal count fell to 198 transactions, marking the lowest quarterly level since 2018, as per PitchBook. More notably, deal value increased 23.2% YoY even as deal count declined 23.6%, highlighting a growing divergence between capital deployment and the number of companies receiving investment.

Figure 1: Global Cybersecurity VC Deal Activity

Source: PitchBook, data as of March 31, 2026

For investors, this suggests the sector is moving into a more concentrated funding environment. Rather than retreating from cybersecurity, venture firms appear increasingly willing to back a narrower group of companies with stronger revenue traction, differentiated technology, and clearer pathways to scale. The result is a market where capital remains available but increasingly reserved for perceived category leaders.

AI-Native Security Companies Reshape Early-Stage Funding

A significant development during the quarter was the shift in funding activity toward early-stage companies. Early-stage cybersecurity investments reached $2.1 billion across 60 deals, surpassing late-stage funding in total capital raised, which totaled $1.7 billion across 70 deals, as per PitchBook. This marked the first time since 3Q22 that early-stage funding exceeded late-stage activity, driven largely by AI-native startups raising unusually large rounds early in their lifecycle.

This shift does not necessarily indicate a broad-based recovery in early-stage venture investing. Instead, it reflects investor conviction in a select group of AI-focused security companies capable of raising substantial rounds at an early stage of development. For venture investors, the trend suggests that AI-native companies are increasingly blurring traditional stage boundaries, raising larger rounds earlier in their development than previous cybersecurity cohorts.

Read more: Autonomy, Commercialization, and Capital Reshape the Defense Tech Landscape

Security Operations Continues to Lead Investment Activity

Among cybersecurity segments, security operations (SecOps) attracted the highest level of investment activity during the quarter, as per PitchBook. The category generated $1.8 billion across 59 deals and expanded 30.5% QoQ, supported by growing enterprise demand for threat detection, response automation, and AI-enabled orchestration capabilities. The segment also continued attracting investor interest across multiple funding stages.

The funding activity reflects a broader shift in enterprise security spending. As organizations face increasingly complex threat environments, security teams are prioritizing platforms that consolidate visibility and automate response workflows. Funding patterns indicate growing investor preference for platforms positioned at the center of security operations rather than narrower point solutions.

AI is Reshaping Cybersecurity Risk

The Global Cybersecurity Outlook 2026 survey found that 94% of respondents expect AI to be the most significant driver of cybersecurity change in the year ahead. At the same time, 87% identified AI-related vulnerabilities as the fastest-growing cyber risk, reflecting the rapid expansion of AI across enterprise environments and business-critical workflows.

The findings help explain the continued flow of capital into cybersecurity markets. AI is creating new attack surfaces while simultaneously becoming an essential component of modern security defenses. As organizations seek to secure AI models, applications, and workflows, cybersecurity vendors addressing these challenges are likely to remain well-positioned within the broader enterprise software landscape.

Read more: Medtech VC & PE Trends 2026: Investors Prioritize Scale, Liquidity, and Commercial Traction

Category Leaders Continue to Attract Capital

Investor capital continued to concentrate in a handful of large cybersecurity transactions during the quarter. Several of the largest financings included Cyera’s $400 million Series F, Cloaked’s $375 million Series B raise, and Tenex.AI’s $250 million Series B. These transactions illustrate continued investor willingness to commit significant capital to companies addressing data security, identity governance, and security operations platforms.

The mix of companies raising the largest rounds highlights where investors see the strongest long-term demand. These transactions demonstrate continued confidence in platforms addressing foundational enterprise security challenges and supporting increasingly complex digital environments. The breadth of these investments suggests that capital is being deployed across multiple layers of the cybersecurity stack rather than a single category.

Conclusion

The cybersecurity market in 2026 is characterized less by expanding deal activity than by increasing capital concentration. Investors are directing larger amounts of funding toward a smaller group of companies, particularly AI-native cybersecurity providers and security operations platforms. While the broader venture market remains selective, cybersecurity continues to benefit from durable spending priorities and growing AI adoption.

About SG Analytics

SG Analytics (SGA) is a global leader in data-driven research and analytics, empowering Fortune 500 clients across BFSI, Technology, Media & Entertainment, and Healthcare. A trusted partner for lower middle market investment banks and private equity firms, SGA provides offshore analysts with seamless deal life cycle support. Our integrated back-office research ecosystem, including database access, design support, domain experts, and tech-enabled automation, helps clients win more mandates and execute deals with precision.

Founded in 2007, SGA is a Great Place to Work® certified firm with 1,600+ employees across the US, the UK, Switzerland, Poland, and India. Recognized by Gartner, Everest Group, and ISG and featured in the Deloitte Technology Fast 50 India 2023 and Financial Times APAC 2024 High Growth Companies, we continue to set industry benchmarks in data excellence.

Related Tags

Author

Steve Salvius

Head of Investment Banking & Private Equity