Sustainable Investing in Private Markets: Repricing Around Returns and Financial Discipline

Private Equity

April, 2026

Sustainable investing in private markets is undergoing a structural repricing toward returns, discipline, and real asset demand. So, investment activity is shifting from narrative-driven strategies toward infrastructure, data, and financially material outcomes.

Sustainable investing in private markets is also entering a phase of recalibration. Therefore, after a volatile 2025 marked by policy uncertainty and shifting narratives, 2026 is presenting a more stable backdrop. Investment activity now continues, with greater emphasis on returns and more defined approaches to impact. In other words, what appears as a slowdown reflects a transition toward more disciplined capital allocation, as investors reassess the role of sustainability within portfolios.

Read more: Enterprise SaaS in 2026: From Growth to Discipline and AI-Led Monetization

ESG Activity Remains Stable Amid More Measured Positioning

Sustainable investing activity appears largely unchanged, although public ESG positioning has become more measured. The perceived slowdown reflects a strategic adjustment in how sustainability communication proceeds. Only 7% of investors have reduced ESG-related communication, while 23% are tailoring how they present sustainability depending on the audience, as per PitchBook. This trend, often referred to as greenhushing, also suggests adaptation to a more complex operating environment.

Furthermore, sustainability evaluation through its contribution to financial performance is on the rise. After all, investors are prioritizing cost efficiency, operational improvements, and risk mitigation over longer-duration initiatives. This reflects a more selective approach, where ESG considerations are applied to areas with clearer return visibility. In this context, sustainable investing is being assessed less as a differentiator and more as part of core investment analysis.

Read More: Consumer AI in 2026

Infrastructure is Driving Climate Capital Expansion

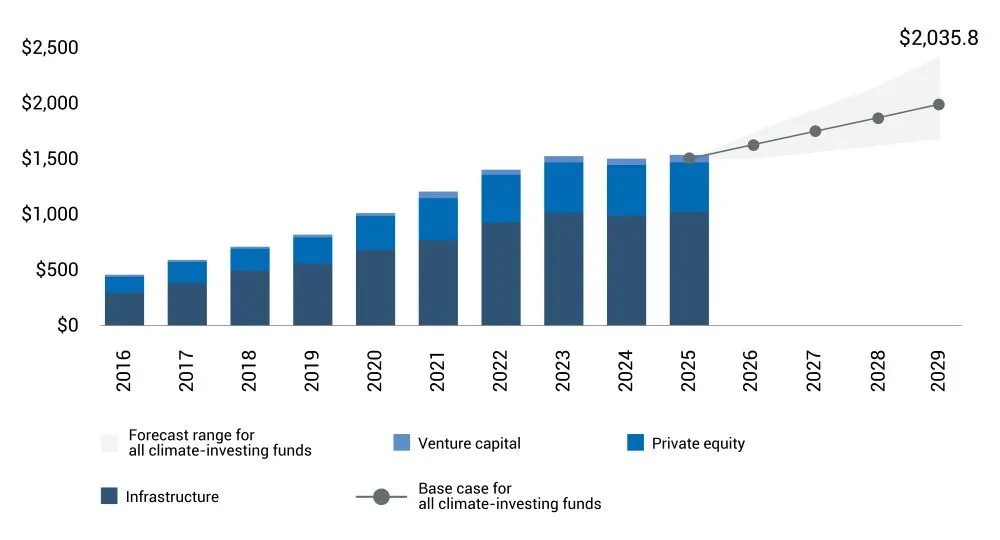

Private market climate AUM reached approximately $1.5 trillion in 2025 and will exceed $2 trillion by the end of the decade, as per PitchBook. At the same time, the composition of that capital appears to be evolving across regions and strategies. Venture capital is losing relative share as macroeconomic conditions continue to affect early-stage investment activity.

Figure 1: Global Private Capital Climate-investing Fund AUM Forecast (in $Billions)

Source: PitchBook, data as of March 31, 2025

Infrastructure has emerged as a primary driver of capital deployment. Energy transition infrastructure funds raised record levels of capital in 2025, with generalist and specialist strategies together attracting over $170 billion. This trend reflects investor preference for stable, cash-generating assets with more predictable risk-return profiles. The energy transition is increasingly being financed through long-duration infrastructure strategies aligned with underlying demand.

Read more: Global M&A Outlook 2026: Capital Repositions for a Structural Era

Institutional Participation Remains Stable as Policy Evolves

Institutional commitment to sustainable investing remains relatively stable despite a more complex policy environment. Around 73% of asset owners continue to integrate sustainability into their investment strategies, a figure that has held broadly consistent in recent years, as per LSEG. This stability persists alongside evolving policy priorities and changing incentive structures, which have introduced additional complexity into investment decisions.

At the same time, the regulatory environment is undergoing a recalibration. Efforts to simplify sustainable finance frameworks are focused on reducing compliance burdens while maintaining transparency. Policy divergence is contributing to regional complexity but does not appear to be disrupting longer-term investment trends. Investors continue to assess sustainability as a factor influencing both risk and return.

Read more: Evergreen Funds Are Becoming the Default Gateway to Private Markets

Financial Materiality is Reshaping ESG Integration

The shift in 2026 is less about whether sustainability is relevant and more about how its evaluation gets reception. Investors are now adopting a materiality-driven approach, focusing on factors with direct financial implications. This transition is due to the improvements in data availability and reporting standards, with 37 jurisdictions representing 60% of global GDP moving toward aligned disclosures, as per LSEG.

This reflects a response to earlier inconsistencies in product labeling and concerns around greenwashing. Investors are placing greater emphasis on measurable outcomes and verifiable data. Sustainability considerations are central to investment processes, with greater focus on disciplined underwriting and incorporation of ESG factors into valuation and risk assessment.

Energy Demand is Reinforcing Investment Trends

Support for sustainable investing has a lot to do with the underlying economic demand. Energy consumption, particularly from AI-driven data centers, is influencing investment priorities. Data center electricity consumption willl be more than double by 2030, creating substantial demand for additional power capacity, as per the International Energy Agency. The renewable energy sector, with its cost-competitive offerings, is also ready to meet a significant portion of this demand.

This trend extends beyond generation to broader energy systems, including efficiency technologies, grid infrastructure, and alternative power sources. Electric vehicle adoption continues globally, while innovations such as virtual power plants and energy-efficient systems are gaining traction. Clean energy economics are becoming increasingly competitive, with 2026 potentially marking a peak in global energy-related emissions.

Conclusion

The current phase of sustainable investing in private markets will likely be a structural reset. Public positioning has become more measured, investment activity is shifting toward infrastructure and scalable assets, and investors are placing greater emphasis on financial materiality. Underlying drivers such as energy demand and institutional participation remain in place, with sustainability becoming more integrated into portfolio construction.

About SG Analytics

SG Analytics (SGA) is a global leader in data-driven research and analytics, empowering Fortune 500 clients across BFSI, Technology, Media & Entertainment, and Healthcare. A trusted partner for lower middle market investment banks and private equity firms, SGA provides offshore analysts with seamless deal life cycle support. Our integrated back-office research ecosystem, including database access, design support, domain experts, and tech-enabled automation, helps clients win more mandates and execute deals with precision.

Founded in 2007, SGA is a Great Place to Work® certified firm with 1,600+ employees across the US, the UK, Switzerland, Poland, and India. Recognized by Gartner, Everest Group, and ISG and featured in the Deloitte Technology Fast 50 India 2023 and Financial Times APAC 2024 High Growth Companies, we continue to set industry benchmarks in data excellence.

Related Tags

Author

Steve Salvius

Head of Investment Banking & Private Equity