Consumer AI in 2026: From Rapid Adoption to Concentrated Outcomes

Venture Capital

April, 2026

Consumer AI has scaled rapidly, but revenue generation remains limited and concentrated among a few platforms. The next phase will be defined by monetization, distribution control, cost efficiency, and sustainable revenue models.

Consumer AI has moved from rapid adoption to structural evolution. That is why scale is no longer the defining factor. Instead, value creation is the priority. While billions of users engage with AI tools, the market shows uneven revenue generation. There are concentrated usage patterns. Besides, a shift in capital toward a small set of scaled players is evident. For investors, this signals a transition to a more selective phase. As a result, the ability to translate engagement into sustainable economics will separate long-term winners from the rest of the market.

Read more: Global M&A Outlook 2026: Capital Repositions for a Structural Era

Adoption Has Scaled, Monetization Remains Limited

Consumer AI has achieved unprecedented scale, with 61% of US adults using AI in the past six months and global users reaching nearly 1.8 billion, including 500 to 600 million daily users, as per Menlo Ventures. This adoption shows AI is no longer experimental. It is now embedded in everyday behavior, spanning tasks such as writing, research, and routine planning. The speed and breadth of this adoption would typically indicate a strong monetization trajectory.

Despite this scale, consumer AI spending remains around $12 billion, with only about 3% of users paying for premium services, and even leading platforms converting a small share of their base. This gap highlights a fundamental disconnect where usage does not translate into willingness to pay. For investors, this suggests the current phase is defined by engagement without corresponding economic value.

Read more: Enterprise SaaS in 2026: From Growth to Discipline and AI-Led Monetization

Default Behavior is Driving Market Concentration

Consumer behavior in AI is highly centralized, with 91% of users relying on a single general-purpose assistant as their default starting point. This indicates a preference for convenience over specialization, where users return to familiar tools rather than exploring alternatives. As a result, generalist platforms benefit from strong habit formation, reinforcing their position as the primary interface for use cases.

This behavior is already translating into economic concentration. General AI assistants capture 81% of total consumer AI spend, with leading platforms commanding a dominant share of that value, supported by significantly higher engagement and retention metrics. For instance, ChatGPT shows a daily active users to monthly active users (DAU to MAU) ratio of around 36% compared to roughly 21% for Gemini, alongside materially stronger long-term retention, as per Andreesen Horowitz. The market is not evolving into a fragmented ecosystem but into one where a few platforms control both usage and revenue.

Read moe: US Asset Management Outlook 2026 – Competition Beyond Scale

Product Innovation is Outpacing Retention

The consumer AI ecosystem has seen a rapid expansion in product capabilities, with companies launching features across multimodal generation, agents, productivity tools, and standalone interfaces. This reflects an industry still experimenting with form factors to identify where durable consumer value will emerge. Companies are prioritizing breadth of offerings, but consistent engagement across these experiences remains uneven.

Despite this, sustained engagement remains limited for many products. OpenAI’s Sora, for instance, recorded sub-8% retention after 30 days, highlighting the difficulty of converting early user interest into repeat usage, as per Andreesen Horowitz. This indicates that while new product experiences are expanding rapidly, they have yet to translate into sustained engagement. For investors, focus should shift toward identifying products that will likely deliver consistent and repeat usage over time.

Read more: US IPO Outlook 2026: A Market Defined by Scale, Selectivity, and Execution

Capital is Concentrating Around Scaled Platforms

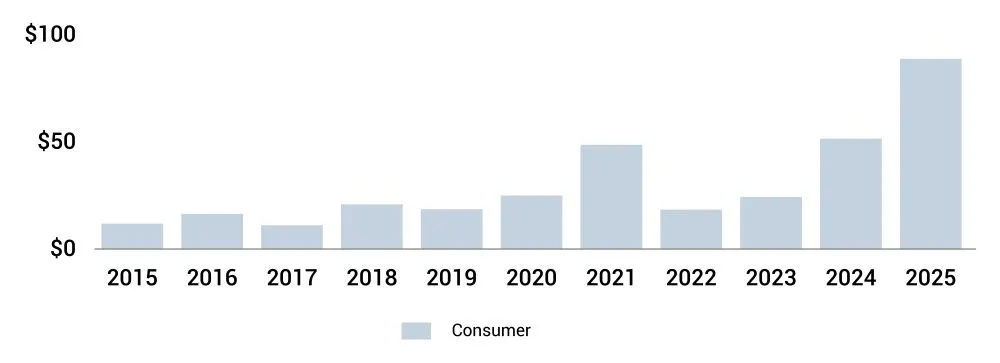

Venture capital activity in consumer AI reflects a clear shift toward scale, with $89 billion invested across 668 deals in 2025, as per PitchBook. While this suggests strong investor interest, the distribution of capital reveals a more concentrated pattern beneath the surface. Deal activity has stabilized, but capital deployment has increased significantly, indicating that investors are prioritizing larger, more established platforms.

Figure 1: Consumer AI VC Deal Value ($ in Billions)

Source: PitchBook, data as of December 31, 2025

The stage-wise distribution of funding reinforces this. Nearly 95% of capital goes to late-stage and venture growth companies, while early-stage participation declines. A small number of megadeals now account for a disproportionate share of total investment. So, they concentrate capital in a handful of players. For investors, this signals a market where scale advantages are being reinforced rather than disrupted.

Read more: Secondaries in Private Markets: A Core Channel for Liquidity and Portfolio Management

Pricing Power, Distribution, and Cost Will Define Returns

As the market matures, companies are testing premium pricing models. Such models can reach up to $200 per month. However, the sustainability of these approaches remains uncertain given current user behavior, as per PitchBook. This highlights a broader challenge where willingness to pay has not kept pace with the perceived utility of AI tools.

At the same time, distribution and cost structures are becoming critical. Rising customer acquisition costs are increasing the importance of embedded distribution channels. Meanwhile, application-layer companies continue to face margin pressure due to underlying model costs. For investors, long-term returns will depend on identifying companies that will likely efficiently acquire users, sustain pricing power, and manage cost structures at scale.

Conclusion

Consumer AI is entering a phase where scale alone is no longer sufficient to define success. The concentration in both usage and capital shapes the market. At the same time, persistent gaps in monetization and retention highlight the challenges ahead. Therefore, for investors, the focus must shift from identifying growth stories to evaluating which platforms will likely translate scale into sustainable economic value.

About SG Analytics

SG Analytics (SGA) is a global leader in data-driven research and analytics, empowering Fortune 500 clients across BFSI, Technology, Media & Entertainment, and Healthcare. A trusted partner for lower middle market investment banks and private equity firms, SGA provides offshore analysts with seamless deal life cycle support. Our integrated back-office research ecosystem, including database access, design support, domain experts, and tech-enabled automation, helps clients win more mandates and execute deals with precision.

Founded in 2007, SGA is a Great Place to Work® certified firm with 1,600+ employees across the US, the UK, Switzerland, Poland, and India. Recognized by Gartner, Everest Group, and ISG and featured in the Deloitte Technology Fast 50 India 2023 and Financial Times APAC 2024 High Growth Companies, we continue to set industry benchmarks in data excellence.

Related Tags

Author

Steve Salvius

Head of Investment Banking & Private Equity