Tariffs and Turbulence: The Changing Flight Path of Aerospace & Defense

Capital Markets

April, 2025

The aerospace and defense sector (A&D), long regarded as a pillar of economic and geopolitical stability, is now contending with an increasingly complex risk landscape. Escalating trade tensions, shifting fiscal priorities, and evolving international alliances are introducing significant uncertainty for investors.

A Resilient Sector Now Faces Political and Economic Volatility

The aerospace and defense (A&D) sector has traditionally been one of the most stable segments of the global economy. In 2024, defense spending globally topped $2.46 trillion, with the US accounting for a dominant 40%, as per a February 2025 report by IISS. This longstanding strength has historically made the sector a haven for private equity (PE) investors and contractors alike. However, recent developments, including new tariffs and budget realignments, are shaking up the industry, revealing vulnerabilities in what was once considered a fortress of policy and fiscal certainty.

Tariffs imposed by the US and subsequent retaliation from other countries have increased tensions within global supply chains. A&D manufacturing is particularly exposed due to its reliance on high-grade metals such as steel, titanium, and aluminum, many of which are imported. These materials often cross international borders multiple times during the production process, compounding the impact of tariffs. The result is rising costs that threaten profitability and erode the predictability that once defined the sector.

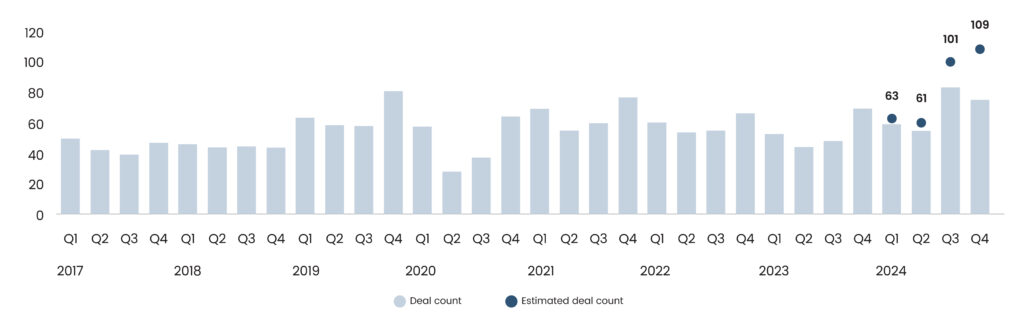

Global A&D PE Deal Count by Quarter

Source: PitchBook, data as of December 31, 2024

Read more: Biopharma Modalities VC Trends: Selective Bets as Investors Seek De-risked Opportunities

PE firms, typically attracted by the sector’s long-term contracts and policy insulation, are now proceeding with caution. While deal activity remained high through late 2024, Pitchbook expects a slowdown in dealmaking in Q1 and Q2. This is not due to a lack of capital or opportunity but rather investor unease surrounding trade policy volatility and domestic defense budget changes.

Defense Budget Cuts Add a Domestic Layer of Complexity

In addition to global trade pressures, US domestic policy shifts are introducing new uncertainties. In February 2025, the Trump administration announced plans to cut $50 billion, approximately 8%, from the defense budget for fiscal year 2026. These reductions are part of a broader strategy to fund priorities like border security and the domestic missile defense initiative. This move marks a stark shift from the traditionally sacrosanct status of the US defense budget and is already causing concern among defense contractors and their financial backers.

Such cuts affect more than just immediate revenues, as they disrupt the long-term capital planning on which defense firms rely. Programs tied to environmental research, diversity initiatives, or multilateral partnerships will likely be most vulnerable, reflecting a shift in defense philosophy. For firms built around stable, multi-year government contracts, these kinds of unpredictable reallocations are deeply problematic, complicating both operations and strategic planning.

Meanwhile, European allies are re-evaluating their procurement strategies. In March 2025, the EU launched its €800 billion “ReArmEurope Plan,” aimed at boosting local defense manufacturing and reducing reliance on US defense exports. With the EU currently sourcing 63% of its defense equipment from the US, this shift is significant. Canada, too, is exploring alternatives to US suppliers, reinforcing the trend toward defense self-sufficiency among longstanding allies.

Geopolitical Shifts Are Reshaping Global Defense Markets

While the US attempts to hold onto its dominant position in the global defense ecosystem, allies are increasingly signaling their intent to diversify. Countries including France, Germany, the UK, and Canada are actively supporting local suppliers to reduce foreign dependency. This move is not purely economic but also strategic. For these nations, bolstering domestic defense capabilities enhances sovereignty and reduces vulnerability to foreign policy shifts in Washington.

The US has not responded quietly. In a March 2025 diplomatic meeting, Secretary of State Marco Rubio warned Baltic leaders that sidelining US defense companies could strain diplomatic ties. Yet the trajectory is clear: as US policies become more unpredictable, allies are less willing to concentrate their defense spending with US firms. This transition will result in significant revenue reallocation from US contractors to firms based in Europe, Canada, South America, and Asia. For PE, this represents both a risk and an opportunity. Investment theses will likely need to be reworked, especially for firms overly exposed to domestic contracts or international sales tied closely to US foreign policy.

The Path Forward: Strategy, Flexibility, and Regional Focus

Uncertainty, not just cost, is the A&D sector’s biggest obstacle in 2025. The challenge lies in balancing immediate risk management with long-term investment. Strategic hedging through localized sourcing, long-term supplier agreements, and regional diversification will be essential to navigate challenges effectively. PE players will also need to rethink their due diligence frameworks. Today’s assessments must account for political exposure, trade route complexity, and a company’s adaptability to policy change.

Read more: The AI Boom is Breathing New Life into Robotics Startups

Nevertheless, the sector’s long-term fundamentals remain compelling. Geopolitical instability in Ukraine, the Middle East, and the Indo-Pacific continues to drive demand for advanced weaponry, surveillance systems, and cybersecurity tools.

About SG Analytics

SG Analytics (SGA) is a global leader in data-driven research and analytics, empowering Fortune 500 clients across BFSI, Technology, Media & Entertainment, and Healthcare. A trusted partner for lower middle market investment banks and private equity firms, SGA provides offshore analysts with seamless deal life cycle support. Our integrated back-office research ecosystem, including database access, design support, domain experts, and tech-enabled automation, helps clients win more mandates and execute deals with precision.

Founded in 2007, SGA is a Great Place to Work® certified firm with 1,600+ employees across the U.S., the UK, Switzerland, Poland, and India. Recognized by Gartner, Everest Group, and ISG and featured in the Deloitte Technology Fast 50 India 2023 and Financial Times APAC 2024 High Growth Companies, we continue to set industry benchmarks in data excellence.

Related Tags

Author

SGA Knowledge Team