Global Private Markets Fundraising Enters a More Selective Cycle in 2026

Private Equity

June, 2026

Private markets fundraising is showing signs of recovery, but capital is returning selectively rather than broadly. Investors are concentrating commitments around established managers, scalable platforms, and long-term growth themes that offer stronger visibility on performance and liquidity.

The private markets fundraising environment entered 2026 with improving momentum despite pressure on fundraising activity. Investor conviction is returning to select areas of the market, particularly around established managers and long-term growth themes. Rather than lifting all managers and asset classes equally, investor preference is increasingly shifting toward established platforms, long-term growth themes, and regions with the strongest investment ecosystems.

Private Markets Remain Resilient Despite Fundraising Pressures

Fundraising levels remain below historical norms across private markets. Global private capital fundraising declined 15.5% YoY to $1.23 trillion, while fund count fell 45.1% to 2,613 vehicles, as per PitchBook. Private equity (PE) fundraising also remained under pressure, extending a multiquarter slowdown that began as higher interest rates and weaker exit activity reduced capital recycling across the market.

Beneath these figures, signs of stabilization are emerging. Private market AUM continues to expand even as fundraising remains subdued, and a growing share of portfolio value is concentrated in older funds awaiting exits. As exit conditions gradually improve, managers will likely gain greater flexibility to return capital and launch successor vehicles. These trends suggest market conditions are improving even though fundraising volumes remain subdued.

Read more: Secondaries in Private Markets: A Core Channel for Liquidity and Portfolio Management

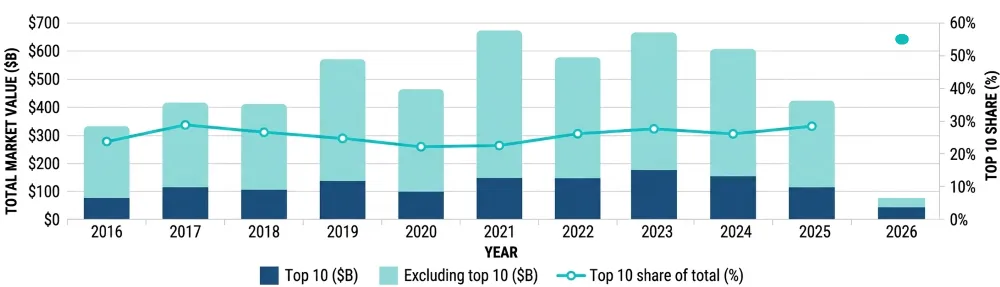

LPs Are Concentrating Capital Around Established Managers

Fundraising success is becoming increasingly concentrated among established managers. More than half of all PE capital raised during 1Q was captured by the ten largest funds, compared with a long-term average of 26.8%. Venture capital displayed a similar trend, with experienced managers securing 83.5% of global commitments as LPs favored familiarity and proven execution over emerging-manager risk.

Figure: Top 10 Funds’ Share of Total PE Capital Raised

Source: PitchBook, data as of March 31, 2026

Investors are increasingly consolidating commitments around firms with strong track records, broad product platforms, and established relationships. This preference reflects a growing emphasis on execution certainty as LPs navigate a more selective fundraising environment. As a result, larger managers continue to strengthen their fundraising advantage while competition for capital intensifies elsewhere.

AI and Private Credit Are Reshaping Capital Allocation

Investor capital is increasingly flowing toward long-term structural opportunities rather than cyclical market trades. Artificial intelligence (AI) has emerged as a major investment theme, with 63% of institutional investors identifying it as the most important trend shaping allocation decisions over the next five years, as per PitchBook. Interest extends beyond software into datacenters, semiconductors, energy infrastructure, and digital connectivity assets.

These themes are already shaping investor allocations. Real assets fundraising increased 25.2% YoY to $172.1 billion, making it one of the strongest-performing strategies globally. Private credit attracted $219.4 billion in fundraising activity. Looking ahead, PitchBook expects private market AUM to grow from $20.3 trillion in 2025 to $26.7 trillion by 2030, supported by private credit, secondaries, evergreen vehicles, and AI-related investment themes.

Read more: Private Credit in 2026: Underwriting Discipline Becomes the Differentiator

Fundraising Execution is Showing Signs of Recovery

Although fundraising volumes remain below prior-cycle highs, fundraising conditions have improved considerably. Funds reaching final close in 1Q26 spent just over 14 months to close, compared with roughly 19 months in 2025, as per PEI. This suggests that LPs are becoming more decisive once they identify managers and strategies that fit their allocation priorities.

Fundraising outcomes also point to stronger investor confidence. More than 80% of funds closing during the quarter either met or exceeded their fundraising targets. At the same time, the share of funds closing below target fell to 19%, down from 35% in 2025 and 42% in 2024. While investors remain selective, they are demonstrating a greater willingness to commit capital when conviction is high.

North America Continues to Lead Global Fundraising

The fundraising recovery remains heavily concentrated in North America. Funds focused on the region raised $92.6 billion during 1Q, comfortably outpacing every other geography, as per PEI. Moreover, multi-regional vehicles followed with $67.4 billion, while Europe raised $24.1 billion and Asia-Pacific attracted just $5.9 billion. These figures highlight the continued preference for markets with deeper capital pools and stronger deployment opportunities.

North America’s leadership is further supported by several of the year’s largest fundraisers. KKR North America Fund XIV raised $23 billion, exceeding its target and becoming the largest close of the quarter. More broadly, accounting for 38% of all capital raised during Q1. Investor demand continues to favor established markets that offer greater scale, liquidity, and visibility into future investment opportunities.

Conclusion

Private markets fundraising is gradually stabilizing, but the recovery remains highly selective. Capital is flowing toward experienced platforms, future-focused investment themes, and regions with proven fundraising ecosystems. For GPs and LPs alike, success in the next phase of the cycle will depend on discipline, differentiation, and long-term strategic positioning. Selectivity is expected to remain a defining characteristic of fundraising activity.

About SG Analytics

SG Analytics (SGA) is a global leader in data-driven research and analytics, empowering Fortune 500 clients across BFSI, Technology, Media & Entertainment, and Healthcare. A trusted partner for lower middle market investment banks and private equity firms, SGA provides offshore analysts with seamless deal life cycle support. Our integrated back-office research ecosystem, including database access, design support, domain experts, and tech-enabled automation, helps clients win more mandates and execute deals with precision.

Founded in 2007, SGA is a Great Place to Work® certified firm with 1,600+ employees across the US, the UK, Switzerland, Poland, and India. Recognized by Gartner, Everest Group, and ISG and featured in the Deloitte Technology Fast 50 India 2023 and Financial Times APAC 2024 High Growth Companies, we continue to set industry benchmarks in data excellence.

Related Tags

Author

Steve Salvius

Head of Investment Banking & Private Equity