Private Credit and Perpetual Capital Drive Public GPs’ Strategic Shift

private credit

June, 2025

With realizations falling sharply in 1Q25, public GPs are re-architecting their models to prioritize stability and recurring income. In turn, private credit and perpetual capital are emerging as core pillars of long-term strategy, not temporary market responses.

Public alternative asset managers are navigating a phase of suppressed realizations, selective fundraising, and market-wide risk aversion. In response, the Big Seven GPs (Blackstone, KKR, Apollo, Carlyle, Ares, TPG, and Blue Owl) are reshaping how they scale and monetize capital. In 1Q25, they focused on expanding private credit and perpetual capital. For public GPs, these aren’t tactical hedges. They are long-term mechanisms to regain operating leverage in a more cautious market.

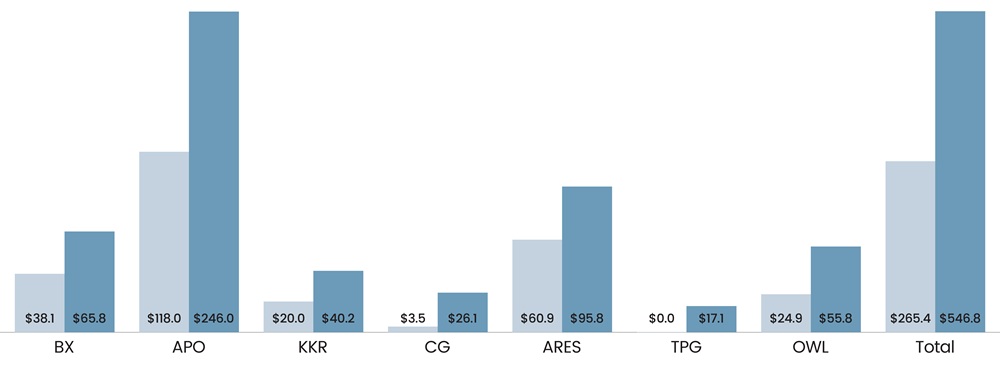

Private Credit Takes the Lead in Deployment

Public GPs deployed $546.8 billion in private credit over the TTM ending 1Q25, nearly double the volume from the year prior, as per PitchBook. Credit has become the most actively deployed asset class across the Big Seven, surpassing both private equity (PE) and other asset classes. Its appeal lies in its speed, scalability, and income potential, making it well-suited in a market constrained by exit delays.

Figure 1: Global TTM Private Credit Deployed by Public GPs (in $Billions)

Source: PitchBook, data as of March 31, 2025

Firms are scaling direct lending and origination platforms to build stable, fee-generating businesses. Unlike equity, credit deployment is less dependent on exit timing, offering a more predictable path to AUM and earnings growth. With investor preferences shifting toward capital preservation and yield, credit is increasingly central to the public GP model in 2025.

Credit Returns Surpass PE

The surge in credit is not just about volume; it is also about returns. The median TTM return for credit strategies reached 13.3%, outperforming the 10.0% median for PE, as per PitchBook. Leading managers are replicating equity-like returns through structured, senior-secured lending with built-in downside protection. Apollo, Ares, and KKR exemplify this shift, scaling investment-grade lending while maintaining strong yields. As allocators reassess volatility exposure, the stability and resilience of private credit are driving increased institutional demand.

Read More: Evergreen Funds in 2025: Growth, Gaps, and the Case for Caution

Perpetual Capital Reaches New Highs

Perpetual capital across the Big Seven reached $1.7 trillion in 1Q25, rising 20.5% YoY and now representing 41% of total AUM, as per PitchBook. According to the McKinsey Global Private Market Report 2025, GPs are increasingly adopting evergreen fund structures, insurance-linked capital platforms, and core real estate strategies, attracted by the stability of NAV-based recurring fees. These structures ease redemption pressures and enable greater control over capital deployment. As liquidity management becomes increasingly critical, the shift toward long-duration capital reflects a deliberate strategy to establish more resilient, future-oriented funding models.

Private Wealth Drives New Inflows

Retail and high-net-worth investors are becoming a key source for perpetual capital inflows. Blackstone raised $11 billion from its wealth platform in 1Q25 alone, pushing its private wealth AUM beyond $270 billion. These figures now approach the scale of institutional verticals and reflect a permanent shift in distribution dynamics.

KKR’s semiliquid K-Series surpassed $22 billion, while Carlyle and TPG are expanding their offerings tailored to individual investors through dedicated wealth-focused vehicles. To capture this demand, firms are streamlining onboarding, standardizing reporting, and offering tailored liquidity terms. Private wealth has matured into a fully institutionalized channel.

Exit Slowdown and Capital Pacing

Aggregate realizations in 1Q25 dropped to $11.1 billion, down from $22.4 billion in the prior quarter, as per PitchBook. The slowdown underscores the ongoing constraints in traditional monetization channels. At the same time, fundraising continues to consolidate, with LPs extending timelines and narrowing commitments. In this environment, Apollo and Blackstone led perpetual capital inflows, reflecting a broader reallocation toward flexible, long-duration structures that help mitigate pacing pressures and improve revenue visibility.

Insurance Capital Is the New Cornerstone

The growth of perpetual capital has been driven in part by insurance platforms. Apollo leads with $403 billion in insurance AUM via Athene and Athora, while Blackstone, KKR, and Ares have also expanded significantly. Insurance capital aligns with long-duration credit and infrastructure strategies and allows GPs to originate assets internally while matching them to liabilities with steady cash flow needs. This model supports recurring revenue, strengthens integration, and improves control over risk-adjusted returns at scale.

The Public GP Model: Designed for Fee-Based Stability

Collectively, these shifts represent more than a tactical reallocation. Public GPs are actively restructuring their business models away from volatile carry and PE realizations and toward fee-related earnings (FRE)-driven growth supported by perpetual capital, private credit, and private wealth channels. These strategies are being recognized by both LPs and public markets. For investors watching the evolution of alternatives, this shift is not just a cyclical adjustment. It marks a permanent transformation in how value will be created and compounded across market cycles.

About SG Analytics

SG Analytics (SGA) is a global leader in data-driven research and analytics, empowering Fortune 500 clients across BFSI, Technology, Media & Entertainment, and Healthcare. A trusted partner for lower middle market investment banks and private equity firms, SGA provides offshore analysts with seamless deal life cycle support. Our integrated back-office research ecosystem, including database access, design support, domain experts, and tech-enabled automation, helps clients win more mandates and execute deals with precision.

Founded in 2007, SGA is a Great Place to Work® certified firm with 1,600+ employees across the U.S., the UK, Switzerland, Poland, and India. Recognized by Gartner, Everest Group, and ISG and featured in the Deloitte Technology Fast 50 India 2023 and Financial Times APAC 2024 High Growth Companies, we continue to set industry benchmarks in data excellence.

Related Tags

Author

Steve Salvius

Head of Investment Banking & Private Equity