Behind the Headlines of US Venture Capital 1Q25

Venture Capital

May, 2025

US venture capital (VC) activity in 1Q25 remained highly concentrated, with AI deals dominating both capital and headlines. Yet beneath the surface, liquidity stayed tight, valuations fragmented, and returns increasingly dependent on fundamentals rather than market hype.

Capital Concentration in AI

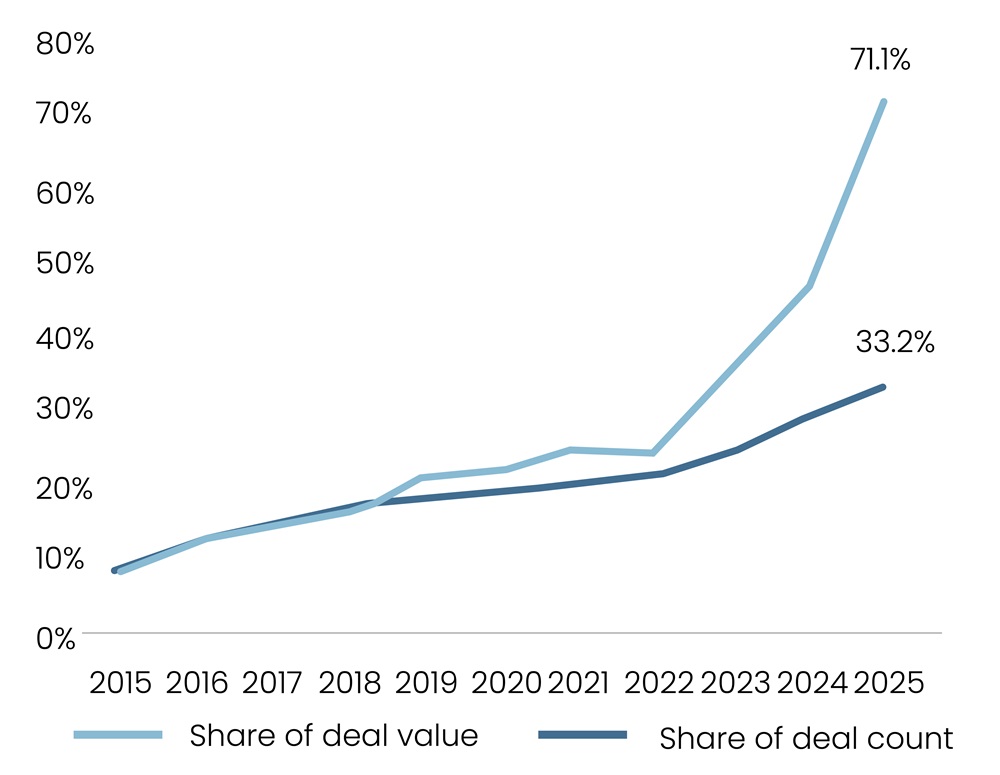

According to PitchBook, in 1Q25, AI and machine learning companies attracted 71.1% of the total US VC deal value. This surge was driven by high-profile transactions, including OpenAI’s $40 billion raise and Anthropic’s valuation expansion from 42.2 billion in January to 61.5 billion by early March. Moreover, the five largest deals of the quarter were all in this segment, reinforcing the extent to which investor appetite is concentrated around a few firms.

Figure 1: AI and ML VC Deal Activity in the US

Source: PitchBook, data as of March 31, 2025

This intense concentration has created a two-speed market. A narrow cohort of companies is attracting capital on favorable terms, while others face lengthier fundraising cycles and downward valuation pressure. Non-AI sectors, though active, are contending with a cautious funding environment where thematic momentum outweighs broad-based confidence. For investors, this creates a need to differentiate between inflated sector enthusiasm and durable, long-term opportunity.

Skewed Valuations Mask Market Caution

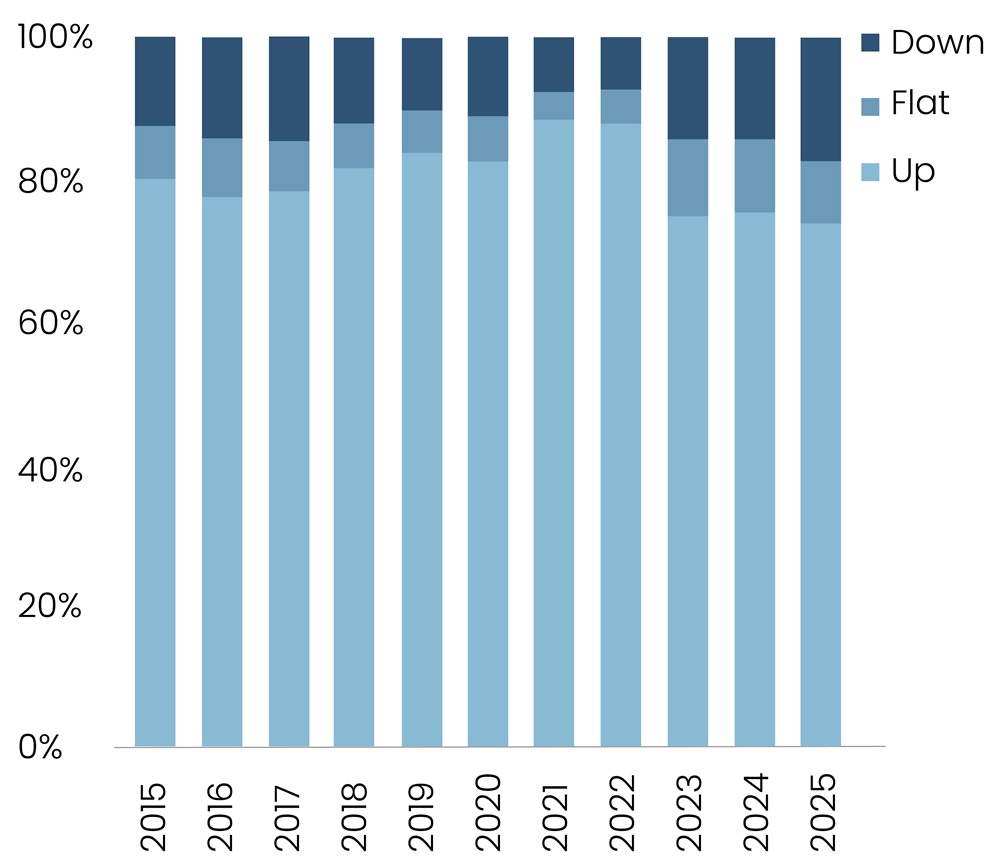

Figure 2: Share of Flat and Down Rounds in US VC Deals

Source: PitchBook, data as of March 31, 2025

Valuation gains in 1Q were largely driven by a handful of outsized AI deals, which skewed medians upward even as broader market sentiment remained subdued. Meanwhile, according to PitchBook, 26.2 percent of all rounds were flat or down, the highest share in more than a decade, signaling continued stress across most of the market. Outside of AI, deal momentum was limited, with muted valuation step-ups and particularly weak pricing power at the late stage, reflecting a constrained environment for mature startups.

Read More: Defense Tech VC: From Frontier to Core Allocation

Liquidity Stays Elusive

Despite a modest uptick in performance, venture returns remain under pressure. According to PitchBook, the one-year rolling internal rate of return (IRR) turned positive in 1Q for the first time in two years. However, this improvement was driven largely by valuation markups rather than actual distributions. Moreover, the median time to exit via IPO has now extended to 6.1 years, the longest stretch since 2016. IPO activity remained limited, with CoreWeave’s listing, one of the few notable exits, underperforming its last private valuation.

EY’s Global IPO Trends report highlights a YoY rise in US IPO volumes in 1Q, with 59 deals raising $8.9 billion. Yet investor sentiment remained hesitant, valuation pressures persisted, and average deal sizes remained modest. Without consistent liquidity, headline IRRs are likely to offer only a temporary signal of recovery. This lack of exit momentum continues to constrain capital recycling, especially for growth-stage companies that are unable to access public markets or attract strategic acquirers.

Investor Strategy Shifts

As investor caution deepens, capital efficiency and operational quality are back in focus. PitchBook notes that step-up multiples for Series D+ deals have declined to 1.2x in 1Q25, nearly half their 2021 peak. As flat and down rounds become more common, investors are increasingly prioritizing fundamentals such as revenue growth, margin discipline, and product-market fit over speculative upside. Startups that cannot demonstrate clear capital productivity or measurable performance milestones are finding it difficult to raise follow-on rounds on favorable terms.

GlobalData reports that US VC funding reached $37.6 billion in 1Q25, marking a YoY increase of more than 50 percent. However, deal volume declined modestly, signaling a more selective approach from investors. This deployment is most visible in Series C rounds, where the Q125 Cooley Venture Financing report shows the deal count dropped from 33 in 4Q to 14 in 1Q. Investors are reinforcing existing positions rather than initiating new exposures, backing companies with stronger metrics and near-term visibility.

Market Outlook and Strategic Positioning

The valuation premium around AI will likely persist in the short term, though capital deployment is likely to become more balanced in the quarters ahead. With dry powder from the 2021–2022 cycle running low, LPs are pressuring returning fund managers for liquidity and disciplined deployment. PitchBook expects fundraising headwinds to intensify unless exit momentum improves. This places pressure on GPs to actively manage portfolios, accelerate value creation, and seek early partial liquidity where possible.

Considering these trends, the investment strategy must evolve. Fund managers and institutional LPs should reassess their allocation toward sectors with stronger unit economics and clearer exit paths. While AI remains a growth engine, underrepresented verticals like healthcare, climate, infrastructure, and enterprise automation will likely offer more compelling risk-adjusted opportunities. Firms that navigate this reset with balanced sector exposure, execution discipline, and capital selectivity will be best positioned to outperform in the next phase of venture investing.

About SG Analytics

SG Analytics (SGA) is a global leader in data-driven research and analytics, empowering Fortune 500 clients across BFSI, Technology, Media & Entertainment, and Healthcare. A trusted partner for lower middle market investment banks and private equity firms, SGA provides offshore analysts with seamless deal life cycle support. Our integrated back-office research ecosystem, including database access, design support, domain experts, and tech-enabled automation, helps clients win more mandates and execute deals with precision.

Founded in 2007, SGA is a Great Place to Work® certified firm with 1,600+ employees across the U.S., the UK, Switzerland, Poland, and India. Recognized by Gartner, Everest Group, and ISG and featured in the Deloitte Technology Fast 50 India 2023 and Financial Times APAC 2024 High Growth Companies, we continue to set industry benchmarks in data excellence.

Related Tags

Author

Steve Salvius

Head of Investment Banking & Private Equity