Artificial intelligence (AI) in 2026 is defined by economic filtering rather than technological novelty. Capital will concentrate around defensible infrastructure, disciplined enterprise deployment, and scalable reasoning systems, while undifferentiated applications face compression and consolidation.

AI has moved beyond experimentation into a phase defined by capital accountability. The global ecosystem now enters a year where capital intensity and enterprise execution determine value creation. Research across advisory firms and investment banks converges on a consistent conclusion that AI in 2026 is less about feature expansion and more about market positioning. Investors must assess capital allocation efficiency and competitive durability across the stack rather than relying on growth momentum.

Read more: Global M&A Outlook 2026: Capital Repositions for a Structural Era

Infrastructure Capital Intensity and the Shift Toward Selectivity

The venture landscape has entered a phase of intensifying competitive pressure across the entire AI stack, marking a significant shift in how capital is deployed and defended. Annual global spending on AI data centers and model training is approaching $1 trillion, reflecting large-scale infrastructure expansion, as per PitchBook. At the same time, AI-assisted development tools have reduced application-layer costs significantly, allowing startups to launch products with limited capital requirements.

This divergence between heavy upstream capital expenditure and low downstream entry barriers creates asymmetric capital exposure. Infrastructure providers carry substantial balance sheet commitments, while application segments face rapid commoditization. Capital intensity and margin pressure are expected to occur simultaneously. For investors, infrastructure exposure requires conviction in scale economics, while application investments must emphasize proprietary data and durable competitive positioning.

Read more: US Capital Markets Outlook 2026: Opportunity in a Return-Driven Cycle

Return Concentration Across the AI Value Chain

Category dispersion is widening. According to PitchBook, foundation models will likely expand from $25.3 billion in 2025 to $136.2 billion by 2030, while AI-driven drug discovery is projected to scale from $1.6 billion to $60 billion over the same period. Enterprise-oriented domains such as customer service automation and AI-native data platforms continue to show demand supported by recurring budget allocations.

In contrast, segments including second-tier medical scribes, generative gaming tools, and consumer assistant applications exhibit feature overlap and limited entry barriers. Margin compression is likely as differentiation narrows. Venture returns are therefore expected to concentrate in platform-grade systems rather than application-layer wrappers. Investors in 2026 must evaluate data ownership, regulatory positioning, integration depth, and ecosystem leverage instead of prioritizing revenue growth in isolation.

Read more: Private Credit in 2026: Underwriting Discipline Becomes the Differentiator

Enterprise AI and the Move Toward Earnings Accretion

Enterprise deployment is shifting from experimentation to a structured, organization-wide operating model redesign. PwC’s 2026 AI Business Predictions indicate that only a limited group of firms currently captures material gains, reflected in measurable revenue acceleration and valuation premiums. Most organizations continue to realize incremental efficiencies that do not materially alter earnings trajectories.

Differentiation depends on governance architecture and execution discipline. Leading firms prioritize high-value workflows, assign senior accountability, and align centralized AI capabilities with operations. Agentic systems are expanding into finance, tax, HR, and supply chain functions, automating complex processes rather than isolated tasks. Capital allocation should favor enterprises demonstrating measurable ROI and disciplined deployment over broad experimentation.

Read more: 2026 US VC Outlook: Early-Stage Strength and AI Momentum

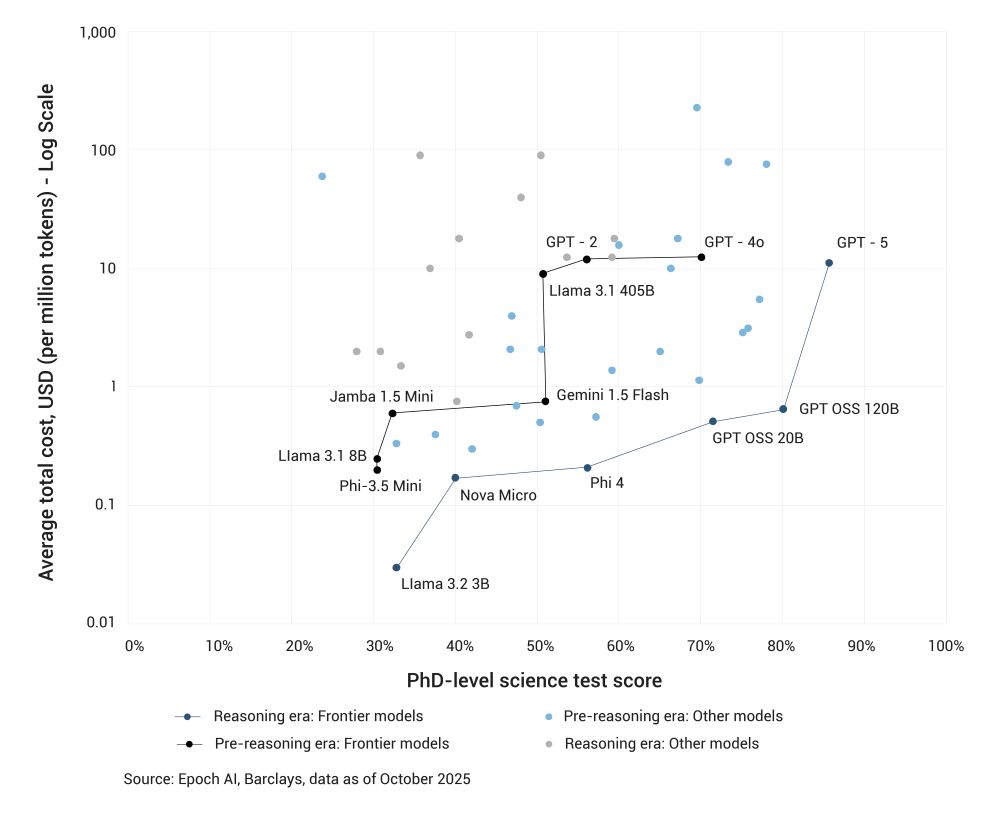

The Unit Economics of Reasoning Models

The technical benchmark for progress is evolving toward economically grounded measurement. Barclays’ AI Outlook 2026 highlights a transition from parameter scale toward reasoning capability and economic utility. Evaluation metrics increasingly reflect real-world job performance, aligning model assessment with productivity outcomes rather than academic benchmarks.

The Downward Shift of the AI Economic Frontier, Driving Cost-Adjusted Performance

Source: Epoch AI, Barclays, data as of October 2025

While training, compute growth is stabilizing, inference intensity per query is increasing as reasoning systems allocate greater computational resources to each task. Architectural approaches such as mixture-of-experts and model distillation improve efficiency, yet cost-per-query remains a critical operating variable. Sustainable valuation requires productivity gains to exceed inference costs. Investors should analyze monetization structure and unit economics rather than assuming technical advancement will sustain premium multiples.

Read more: Global Private Market Fundraising: A Selective Capital Cycle

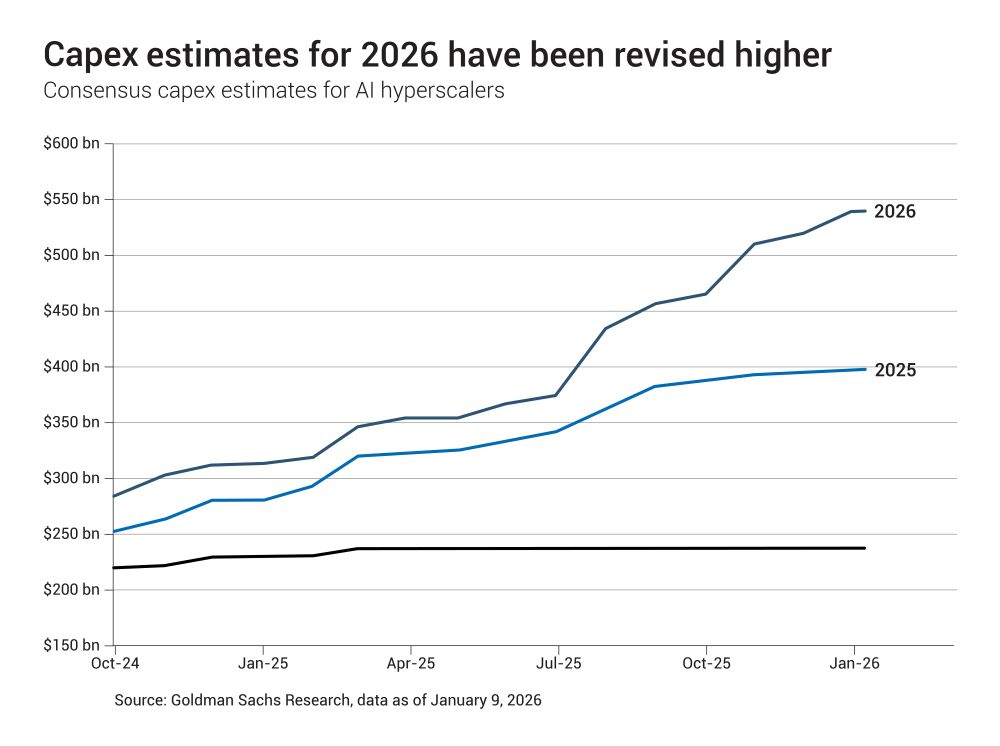

Platform Concentration and Portfolio Exposure Risk

Capital markets reflect industry-wide platform concentration across AI systems. Goldman Sachs projects hyperscale cloud providers will invest over $500 billion in capital expenditures in 2026. The seven largest technology companies account for more than 30% of the S&P 500’s market capitalization and roughly a quarter of its earnings, embedding AI leadership within index concentration.

Source: Goldman Sachs Research, data as of January 9, 2026

Models are increasingly positioned as orchestration layers that coordinate tools autonomously rather than execute static prompts. Control over foundational models resembles ownership of a computing platform layer, reinforcing alliances among infrastructure providers, semiconductor manufacturers, and enterprise software incumbents. Portfolio construction in 2026 must account for both the opportunity and exposure risk inherent in this configuration.

Read Also – Difference Between Debt Capital Markets (DCM) and Equity Capital Markets (ECM)?

Conclusion

AI in 2026 represents a transition from technological expansion to economic selection. Infrastructure investment remains elevated, venture categories are diverging, enterprise deployment is becoming more disciplined, and reasoning economics are reshaping valuation frameworks. Investors who evaluate capital durability and competitive positioning are more likely to generate sustainable returns, while broad thematic exposure without discipline faces compression.

About SG Analytics

SG Analytics (SGA) is a global leader in data-driven research and analytics, empowering Fortune 500 clients across BFSI, Technology, Media & Entertainment, and Healthcare. A trusted partner for lower middle market investment banks and private equity firms, SGA provides offshore analysts with seamless deal life cycle support. Our integrated back-office research ecosystem, including database access, design support, domain experts, and tech-enabled automation, helps clients win more mandates and execute deals with precision.

Founded in 2007, SGA is a Great Place to Work® certified firm with 1,600+ employees across the U.S., the UK, Switzerland, Poland, and India. Recognized by Gartner, Everest Group, and ISG and featured in the Deloitte Technology Fast 50 India 2023 and Financial Times APAC 2024 High Growth Companies, we continue to set industry benchmarks in data excellence.