The US IPO market is entering a more disciplined phase. It now exhibits a resilient recovery, stronger investor selectivity, and a deep backlog of issuers. In 2026, outcomes will be less about market access. Instead, they will be more unique due to scale, sector alignment, and execution readiness.

After two years of uneven recovery, the US IPO market is entering 2026 with greater clarity and discipline. Activity in 2025 confirmed that investor appetite has returned, but not indiscriminately. Markets favored scale, visibility, and credible growth while penalizing speculative narratives. What is emerging is not a broad reopening, but a more structured IPO environment where quality and timing determine outcomes.

IPO Recovery and Deal Scale in 2025

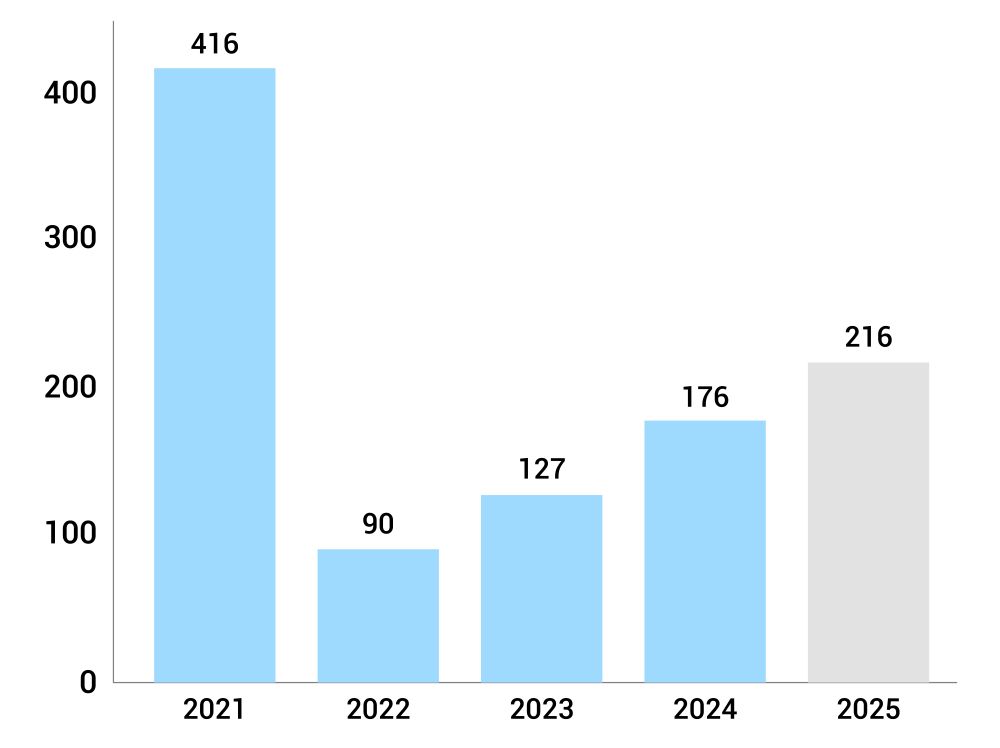

The US IPO market in 2025 continued its rebound, with total deals reaching 216. It proceeds rising to $47.4 billion, reflecting recovery from prior lows, as per EY’s IPO market trends analysis. This progress came despite periods of volatility, yet equity markets remained resilient with multiple record highs. The ability of markets to absorb fluctuations while sustaining issuance reinforced investor confidence and supported the reopening of IPO activity.

Figure 1: Number of IPOs in the US Over the Years

Source: EY Analysis, data as of December 31, 2025

The composition of issuance points to a healthier structure, with larger deals driving activity and a rising share of offerings exceeding $100 million. Technology, media, and telecommunications led issuance, supported by strong participation from technology-led sectors, while healthcare and financial services also contributed. This broad-based sector participation signals that recovery is not narrowly concentrated, positioning 2026 as a continuation of an already stabilized IPO cycle.

Structural Shift Toward Larger and Higher-Quality IPOs

The IPO market has undergone a structural shift, with scale and maturity becoming central to issuance dynamics. IPO volumes rose in 2025, but the average deal size expanded to around $510 million, as per RBC Capital Markets. This increase reflects a market dominated by larger, more established companies, as sponsors held assets longer and brought scaled businesses to public markets rather than earlier-stage issuers.

Investor expectations have evolved alongside this shift, with institutions showing greater selectivity and prioritizing companies with credible growth profiles and execution visibility. Pricing dynamics also tightened, as investors became comfortable with narrower IPO discounts compared to previous years. The result is a market where access is no longer constrained, but successful execution depends on disciplined timing, credible positioning, and meeting a higher quality threshold.

Investor Demand Shaped by AI and Sector Rotation

The demand environment for IPOs in 2026 will be shaped by sector dynamics, with artificial intelligence (AI) remaining central. While AI dominated attention in 2025, investor focus is shifting toward tangible outcomes, with evidence of revenue expansion and efficiencies from adoption. This transition to monetization-led validation is expected to sustain investor appetite for AI-linked companies entering public markets.

At the same time, sector rotation is becoming more pronounced, with healthcare emerging as a key area of investor interest supported by improving valuations and earnings momentum. Investor preferences are also shifting toward growth-oriented opportunities, reflecting changes in capital allocation. These dynamics indicate that IPO demand will not be uniform but concentrated in sectors and companies aligned with prevailing themes.

Backlog of Deferred Listings and Supply Dynamics

The IPO market entering 2026 is being driven by improving macro conditions and deferred issuance from prior years. Companies that delayed listings in favor of private funding are now facing a more stable environment, supported by cooling inflation, declining interest rates, and stronger equity market performance. This shift reduces the incentive to remain private and creates pressure for companies to access public markets.

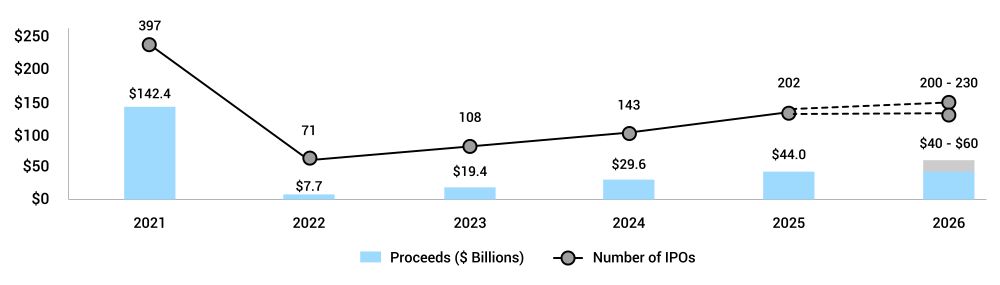

Figure 2: Anticipated Recovery of the IPO Market in 2026

Source: Renaissance Capital

As a result, IPO activity will increase. Projections indicate 200 to 230 IPOs. They will be raising between $40 billion and $60 billion in 2026, as per Renaissance Capital IPO Outlook 2026. This growth reflects improved market conditions and the release of pent-up supply from companies that deferred listings. Venture-backed issuers, particularly those aligned with high-growth themes such as AI, are expected to play a central role in driving this next phase of activity.

IPO Pipeline Depth and Execution Readiness

The current IPO pipeline highlights the depth of supply preparing to enter public markets, with more than 190 companies already filed and targeting over $6 billion in capital, as per Renaissance Capital. This pipeline spans sectors, including technology, industrials, financials, healthcare, and energy, and includes several offerings expected to exceed $100 million. The breadth and scale of this pipeline indicate that the market will show sustained activity.

Beyond public filings, the private market backlog of companies targeting public listing remains substantial. There are over 240 companies that are potential IPO candidates in the near term. This includes names such as OpenAI, SpaceX, Anthropic, Canva, and Revolut, reflecting the scale of companies preparing for listings. However, not all will successfully transition. Execution readiness, timing, and positioning relative to investor demand will determine which companies proceed and which continue to delay.

Conclusion

The US IPO market in 2026 is entering a phase where opportunity is abundant, and the differentiated outcomes are increasing. A resilient 2025, evolving investor expectations, and a deep backlog of companies support higher activity, but not uniform success. Execution quality, preparedness, and alignment with investor demand will determine which IPOs successfully translate market opportunity into performance.

About SG Analytics

SG Analytics (SGA) is a global leader in data-driven research and analytics, empowering Fortune 500 clients across BFSI, Technology, Media & Entertainment, and Healthcare. A trusted partner for lower middle market investment banks and private equity firms, SGA provides offshore analysts with seamless deal life cycle support. Our integrated back-office research ecosystem, including database access, design support, domain experts, and tech-enabled automation, helps clients win more mandates and execute deals with precision.

Founded in 2007, SGA is a Great Place to Work® certified firm with 1,600+ employees across the US, the UK, Switzerland, Poland, and India. Recognized by Gartner, Everest Group, and ISG and featured in the Deloitte Technology Fast 50 India 2023 and Financial Times APAC 2024 High Growth Companies, we continue to set industry benchmarks in data excellence.