The secondary market has evolved into a core structural component of private capital, enabling liquidity, portfolio optimization, and extended asset ownership. Its role now reflects systemic integration within private markets rather than incremental growth or cyclical demand.

The secondary market has entered a more established phase, driven by rising liquidity needs and evolving portfolio management strategies, and remains largely shaped by private equity activity. In 2025, both limited partners (LPs) and general partners (GPs) increasingly relied on secondaries not just as opportunistic tools, but as clear tools to manage capital, rebalance exposure, and extend asset ownership. As private markets continue to scale and holding periods remain elevated, traditional exit routes alone are no longer sufficient to meet liquidity expectations.

Transaction Scale Reflects Market Depth

The secondary market’s expansion in 2025 reflects a clear transition toward institutional scale. Global transaction volume reached $240 billion, representing a 48% YoY increase and marking the highest level recorded to date, as per the Jefferies 2025 Global Secondary Market Review. Activity accelerated significantly in the latter half of the year, with nearly $137 billion of transactions completed during that period alone, indicating sustained demand from both buyers and sellers.

This level of activity reinforces the market’s role as a consistent liquidity channel rather than a reactive one. Investors increasingly used secondaries to address distribution gaps, while sellers used the market to actively manage portfolio allocations. At the same time, rising levels of dedicated secondary capital enabled buyers to absorb larger transactions, supporting their use as a standard allocation tool within private capital frameworks.

Read moe: US Asset Management Outlook 2026 – Competition Beyond Scale

GP-Led Transactions Embedded in Exit Strategies

GP-led transactions now represent a standard component of PE exit strategies rather than an alternative pathway. In 2025, GP-led volume reached $115 billion, accounting for nearly half of total secondary activity and growing 53% YoY, as per the Jefferies Report. This reflects how sponsors are increasingly incorporating secondary structures into their portfolio management approach.

Continuation vehicles are a key mechanism within this segment, enabling sponsors to transfer assets into new vehicles while providing liquidity to existing investors. Adoption has expanded across leading PE firms, with a significant proportion of top sponsors now utilizing these structures. This shift indicates that for high-quality assets, extending ownership through secondaries is increasingly preferred over pursuing traditional exits prematurely.

Pricing Trends Reflect Asset-Level Selectivity

Despite record transaction volumes, pricing trends indicate that the secondary market remains disciplined in its valuation approach. According to Campbell Lutyens’ 2025 Secondary Market Flash Report, average discounts in LP-led transactions widened modestly to 13.9% in 2025, compared with 13.3% in the previous year, reflecting a broader mix of assets being traded and sellers’ willingness to accept discounts in exchange for liquidity.

At the same time, pricing remained resilient for high-quality assets, particularly within established buyout strategies. Leading funds continued to transact at strong valuations, with top-tier assets often pricing close to net asset value or at premiums. This divergence highlights increasing selectivity among investors, reinforcing a more efficient and fundamentals-driven pricing environment within the secondary market.

Read more: Global M&A Outlook 2026: Capital Repositions for a Structural Era

Expanding Capital Pools Broaden the Buyer Base

The expansion of capital allocated to secondaries is another defining feature of the market’s evolution. Evergreen investment vehicles alone have surpassed $100 billion in assets under management, emerging as a significant source of demand across both LP-led and GP-led transactions, as per Campbell Lutyens. This increase reflects sustained investor conviction in secondaries as a core allocation.

Alongside this capital growth, the buyer base is becoming increasingly diversified. While large secondary platforms remain dominant in major transactions, new entrants, specialized investors, and retail-oriented capital are gaining prominence. This broader participation enables the execution of a wider range of deal sizes and structures, reinforcing the market’s ability to support both large-scale and more targeted transactions efficiently.

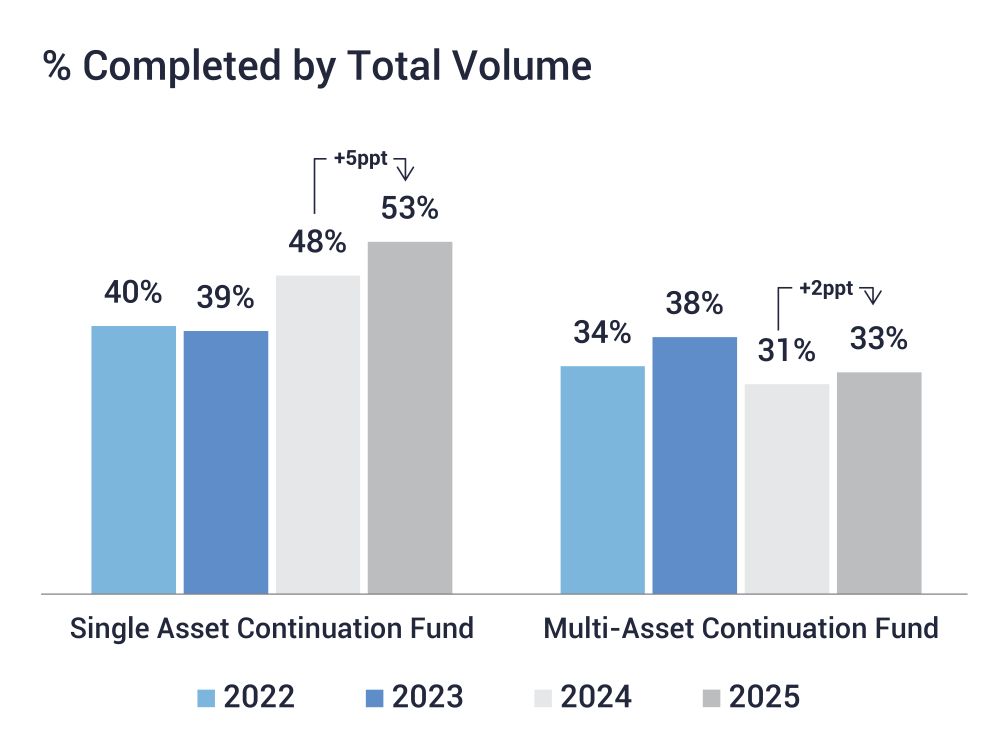

Continuation Structures and Asset-Level Concentration

Continuation-driven structures have become a defining feature of secondary market activity, particularly in how sponsors manage concentrated exposures. Single-asset continuation funds accounted for approximately 53% of continuation vehicle activity, with multi-asset vehicles representing around 33% of total volume, as per the Lazard Secondary Market Report. This distribution reflects a clear preference for retaining high-quality assets while still providing liquidity to existing investors.

Read more: 2026 US VC Outlook: Early-Stage Strength and AI Momentum

Figure 1: Capital Deployment by Transaction Type

Source: Lazard Secondary Market Report 2025

Sponsors and LPs are increasingly integrating these structures into standard portfolio management processes. At the same time, approximately 67% of single-asset deals were priced above 95% of net asset value, indicating sustained demand for high-quality assets. This reinforces the role of secondaries not only as a liquidity tool, but also as a mechanism for disciplined capital allocation and extended ownership.

Conclusion

The secondary market is now firmly established within private capital markets. Record transaction volumes, increasing adoption of GP-led structures, and expanding investor participation show that secondaries are central to how capital is recycled and value is extended. As private markets grow in scale and complexity, secondaries will remain critical to enabling capital recycling across the ecosystem.

About SG Analytics

SG Analytics (SGA) is a global leader in data-driven research and analytics, empowering Fortune 500 clients across BFSI, Technology, Media & Entertainment, and Healthcare. A trusted partner for lower middle market investment banks and private equity firms, SGA provides offshore analysts with seamless deal life cycle support. Our integrated back-office research ecosystem, including database access, design support, domain experts, and tech-enabled automation, helps clients win more mandates and execute deals with precision.

Founded in 2007, SGA is a Great Place to Work® certified firm with 1,600+ employees across the US, the UK, Switzerland, Poland, and India. Recognized by Gartner, Everest Group, and ISG and featured in the Deloitte Technology Fast 50 India 2023 and Financial Times APAC 2024 High Growth Companies, we continue to set industry benchmarks in data excellence.